Fear of losing money is the number one reason many beginners never place their first import order. Others rush in unprepared and lose money unnecessarily. The truth is that most first-order losses are not caused by bad luck — they are caused by avoidable decisions. This guide breaks down how beginners in Zambia can reduce risk and protect their capital when placing a first import order.

Step 1: Understand Why Beginners Lose Money

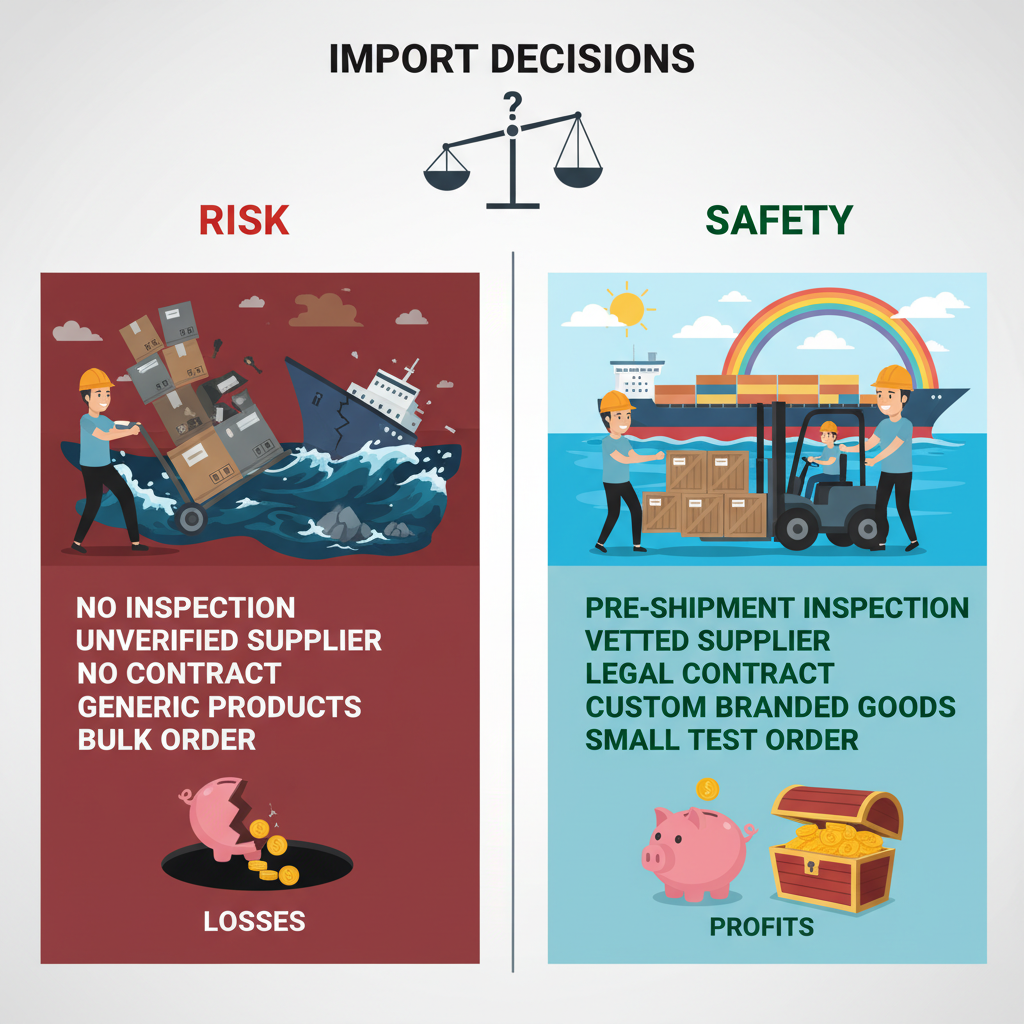

Most first-order losses come from predictable mistakes.

Common causes include:

- Importing too much stock too early

- Choosing products without local demand

- Miscalculating total landed cost

- Trusting suppliers without verification

Understanding these risks upfront helps you avoid repeating them.

Step 2: Start With a Test Order, Not a Bulk Order

Your first order should be a learning order, not a profit-maximising one.

A safe first order:

- Uses a small quantity

- Prioritises testing over margins

- Allows mistakes without major loss

Testing protects capital and builds confidence.

Step 3: Calculate Total Landed Cost Before You Pay

Never send payment before understanding full costs.

You must account for:

- Product cost

- Shipping (air or sea)

- Clearing and customs fees

- Local transport

Ignoring even one cost can erase profit completely.

Step 4: Avoid Emotional Product Choices

Many beginners import products they personally like rather than what sells.

Avoid:

- Trend-driven gadgets

- Products with unclear use

- Items with seasonal demand

Choose products based on demand, not excitement.

Step 5: Verify Your Supplier Before Committing

Supplier mistakes are expensive.

Before paying:

- Check reviews and transaction history

- Ask detailed questions

- Request samples if possible

- Avoid pressure tactics

A reliable supplier reduces risk more than cheap pricing.

Step 6: Plan How You Will Sell Before the Product Arrives

Importing without a sales plan causes panic selling.

Before arrival:

- Know where you will sell

- Set a realistic price

- Prepare simple product explanations

Prepared sellers sell faster.

Step 7: Separate Business Money From Personal Money

Mixing funds hides losses and creates stress.

Best practice:

- Allocate a fixed amount for the order

- Do not dip into personal funds

- Reinvest profits before spending

Clear separation improves decision-making.

Step 8: Accept Small Losses as Learning Costs

Not every first order is perfect.

Smart beginners:

- Learn from small mistakes

- Improve supplier selection

- Adjust pricing and product choice

Small controlled losses prevent big future ones.

Common First-Order Mistakes to Avoid

- Going “all in” on one product

- Skipping samples to save money

- Underpricing to sell quickly

- Copying other sellers blindly

Worried about your first order? Use the first-order safety checklist to reduce risk and import with confidence.